Time Series Note | Financial Time Series Analysis

1. Introduction to Time Series in Python

Time Series is a sequence of information which attaches a time period to each value

- A common topic in Time Series Analysis is determining the stability of financial markets and the efficiency protfolios (效率投资组合)

Properties

All time-periods must be equal and clearly defined, which would result in a constant frequency

- Frequency: how often values of the data set are recorded

- if the intervals are not identical => dealing with missing data

Time-Dependency(时效性): the values for every period are affected by outside factors and by the values of past periods

- in chronological order

- from a machine learning perspective, this is inconvenient for train/test data split

- we need pick a cut-off point and let the period before the cut-off point be the training set and the period after the cutoff point be the testing set

Python Implementation

Step1: Import the library and read the file

- Create a copy of original data in case we erase certain values and read the csv file again

df.head()shows the information of the top five observations for the data set

|

|

Output:

date: represents the day when the values of the other columns (closing prices of four market indexes) were recorded- Each market index is a portfolio of the most traded companies on the respective stock exchange markets:

spx: S&P 500 measures the stability of the US stock exchangesdax: DAX 30 measures the stability of the German stock exchangesftse: FTSE 100 measures the stability of the London Stock exchangesnikkei: NIKKEI 225 measures the stability of the Japanese stock exchanges

Step2: Transform “dd/mm/yyyy” format to “yyyy-mm-dd” datetime format

- set

dateas index:inplace = Truelets date replace the integer index- Once “date” becomes an index, we no longer save/modify its values as a seperate attribute in the data frame

- set frequency:

- arguments: ‘h’ - hourly, ‘w’ - weekly, ’d' - daily, ’m' - monthly

- not interested in any weekends or holidays => missing values NaN

- ‘b’ - business days

|

|

Output:

Step3: Handling Missing Values

- For each attribute,

df_comp.isna().sum()will show the number of instances without available information for each column - Setting the frequency to “business days” must have generated 8 dates, for which we have no data available

fillna()method:- front filling: assigns the value of the previous period

- back filling: assigns the value for the next period

- assigning the same average to all the missing values (bad approach)

|

|

Step4: Adding and Removing Columns

- just keep the index

timeandspxasmarket_value

|

|

Step5: Splitting the Time-Series data

- since time series data relies on keeping the chronological order of the values

- cannot “shuffle” the data before splitting

Training Set: From the beginning up to some cut off pointTesting Set: From the cut off point until the end80-20split is resonable- training set too large: performs poorly with new data

- training set too small: cannot create an accurate model

iloccomes fromindex locationlencomes fromlengthintensures that thetrain_sizewill be integer

|

|

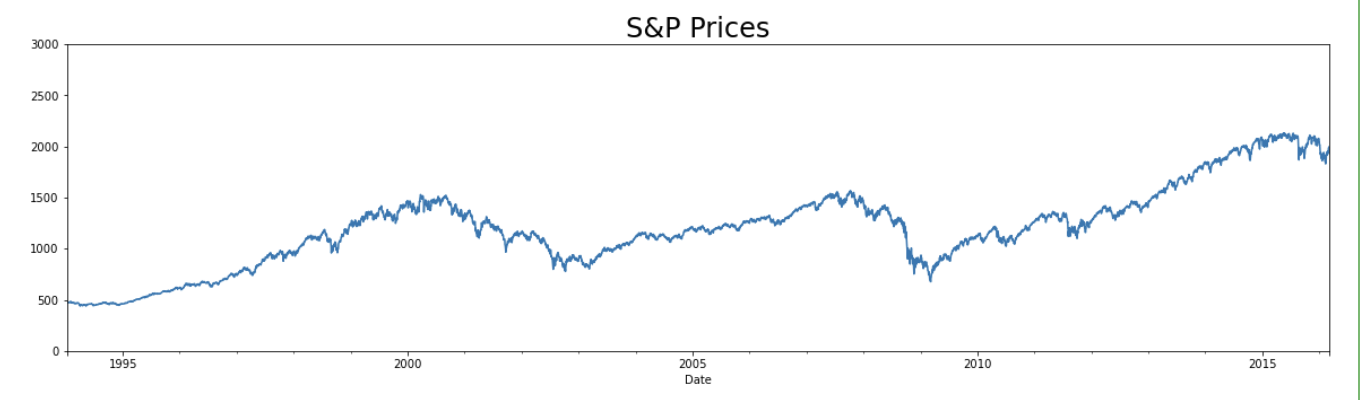

Step6: Data Visualization

|

|

Output:

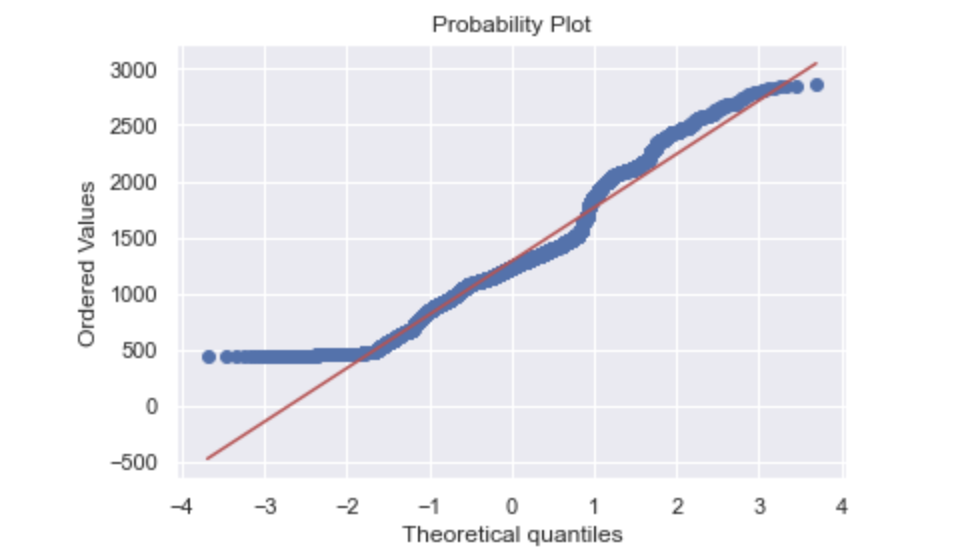

The QQ Plot is a tool used to determine whether a data set is distributed a certain way (normal)

|

|

Output:

Explanation:

- QQ plot takes all the values and arranges them in accending order.

- y represents how many standard deviations away from the mean

- The red diagonal line represents what the data points should follow if they are Normal Distributed

- In this case, since more values are arond 500, the data is not normally distributed

- and we cannot use the elegant statistics of Normal Distributions to make successful forecasts

Extra Step: Scrape the real-time data off of Yahoo Finance

|

|

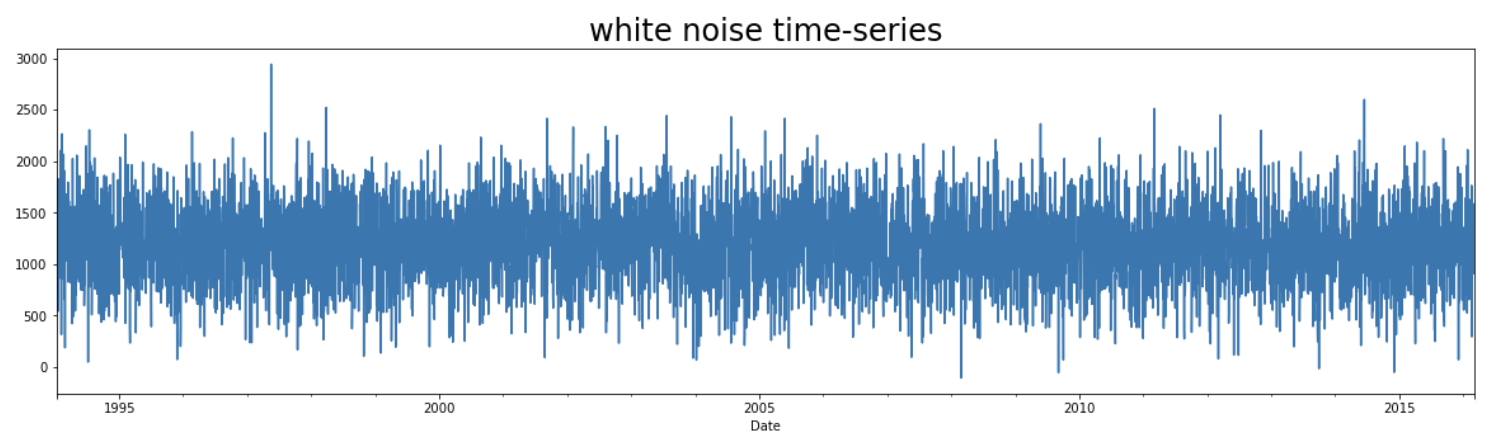

3. White Noise

Definition: A sequence of random data, where every value has a time-period associated with it

- it behaves sporadically, not predictable

Conditions:

- constant mean $\mu$

- constant variance $\sigma^2$

- no autocorrelation in any period: NO clear relationship between past and present values

- autocorrelation measures how correlated a series is with past versions of itself

- $\rho = corr(x_t,x_{t-1})$

Generate White Noise data and plot its values

- compare with the graph of the

S&Pclosing prices

|

|

Output:

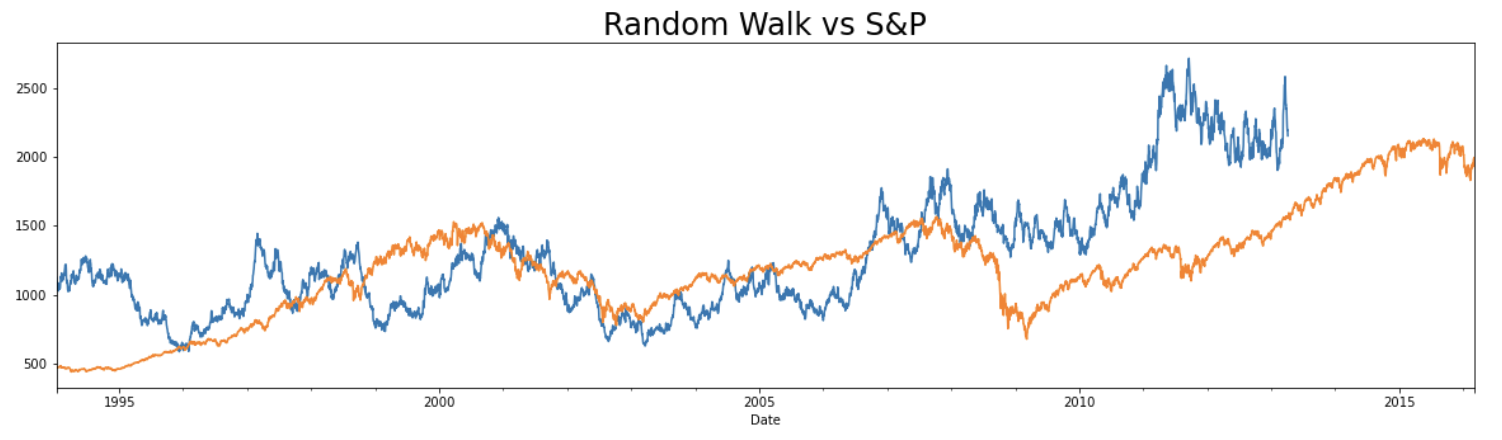

4. Random Walk

Definition: A special type of time-series, where values tend to persist over time and the differences between periods are simply white noise

- $P_t = P_{t-1} + \epsilon_t$, where the residual $\epsilon_t \sim WN(\mu,\sigma^2)$

The random walk data is much more similar to S&P prices than to white noise values

- both have small variations between consecutive time periods

- both have cyclical increases and decreases in short periods of time

|

|

Output:

Market Efficiency: measures the level of difficulty in forecasting correct future values

- in general, if a time series resembles a random walk, the prices can’t be predicted with great accuracy

- conversely, if future prices can be predicted with great accuracy, then there are arbitrage opportunities

- we can speak of arbitrage when investors manage to buy and sell commodities and make a safe profit while the price adjusts

- if such opportunities exist within a market, investors are bound to take advantage, which would eventually lead to a price that matches the expected one, as a result, prices adjust accordingly

5. Stationarity

Strict Stationarity

Rarely observed in nature

- $(x_t,x_{t+k}) \sim Dist(\mu, \sigma^2)$

- $(x_{t+a},x_{t+a+k}) \sim Dist(\mu, \sigma^2)$

Weak-form/Covariance Stationarity

Assumptions:

- Constant $\mu$

- Constant $\sigma^2$

- $Cov(x_n,x_{n+k}) = Cov(x_m, x_{m+k})$

- consistent covariance between periods at an identical distance

Dickey-Fuller Test: to check whether a data set comes from a stationary process

- Null Hypothesis: assumes non-stationarity

- autocorrelation coefficient $\varphi < 1$

- Alternative Hypothesis: $\varphi = 1$

- reject the Null if

test statistic<critical valuein the D-F Table- stationarity

|

|

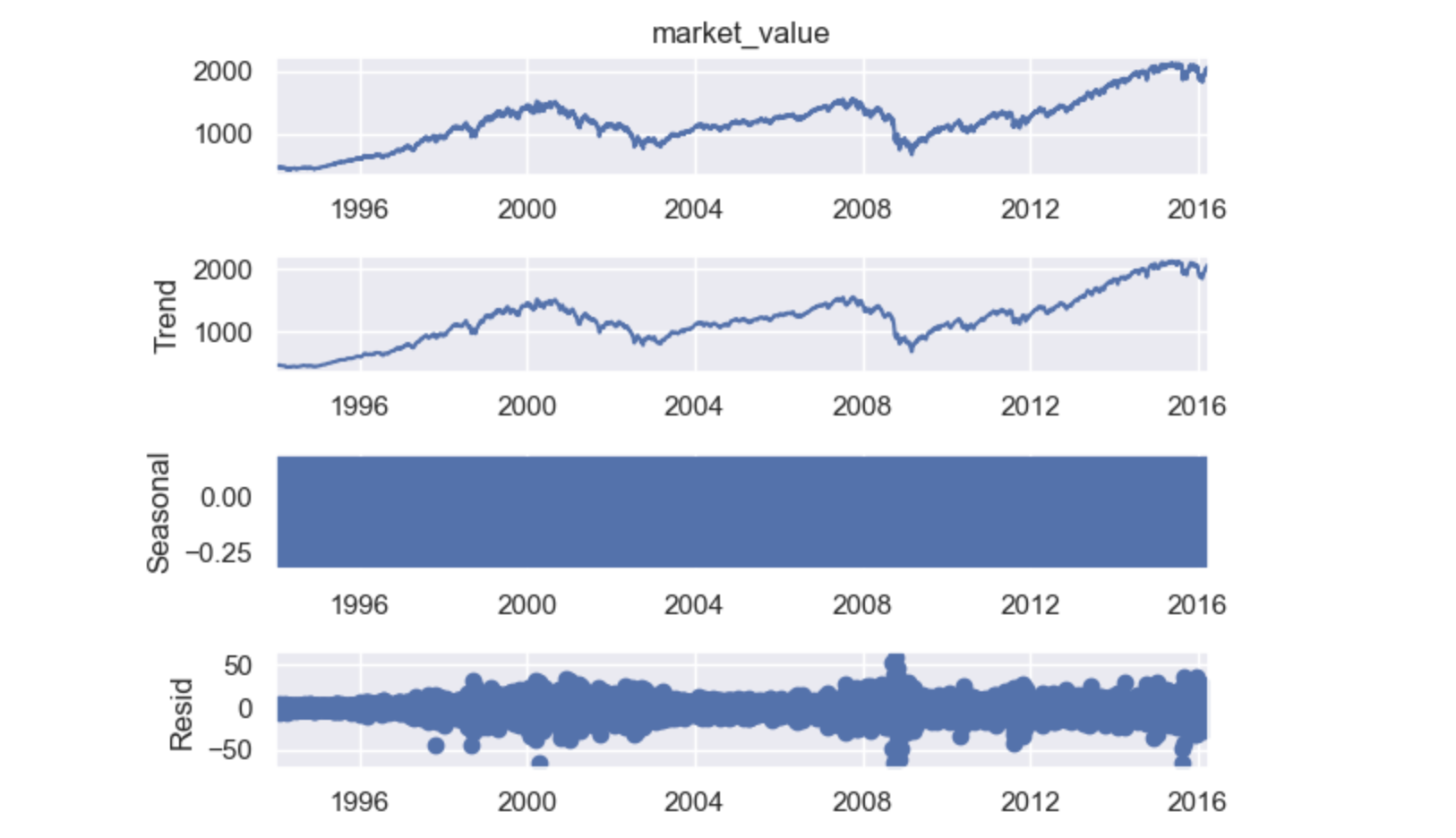

6. Seasonality

Trends will appear on a cyclical basis.

Ways to test for seasonality:

- Decompose the sequence by splitting the time series into 3 effects:

- Trend: represents the pattern consistent throughout the data and explains most of the variability of the data

- Seasonal: expresses all cyclical effects due to seasonality

- Residual: the difference between true values and predictions for any period

Naive Decomposition: Decomposition function uses the previous period values as a trend-setter.

- Additive: observed = trend + seasonal + residual

- Multiplicative: observed = trend x seasonal x residual

|

|

Both Output:

The residuals vary greatly around 2000 and 2008,

- this can be explained by the instability caused by the

.comandhousing pricesbubbles respectively

Seasonal looks like a rectangle:

- values are constantly oscillating back and forth and the figure size is too small

- no concrete cyclical pattern

- => no seasonality in the S&P data

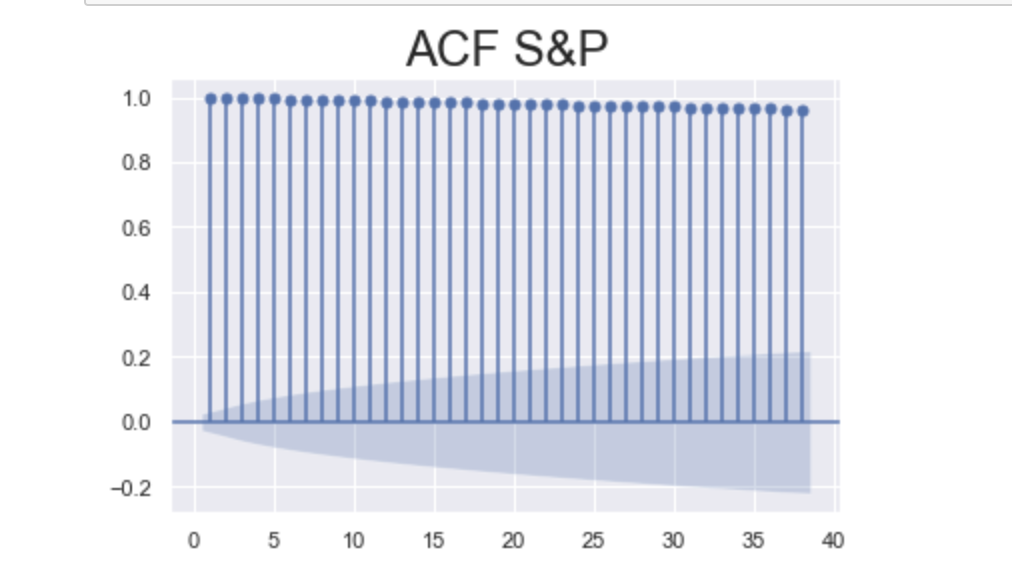

7. The Autocorrelation Function (ACF)

Correlation measures the similarity in the change of values of two series

- $\rho(x,y)$ only have a single variable

Autocorrelation is the correlation between a sequence and itself

- measures the level of resemblance between a sequence from several periods ago and the actual data

Laggedis a delayed series of the original one- how much of yesterday’s values resemble today’s values, or similarities from year to year

ACF for S&P market value

|

|

Output:

Explanation:

- x-axis: represents lags,

- y-axis: indicates the possible values for the autocorrelation coefficient

- correlation can only take values between -1 and 1,

- lines across the plot represent the autocorrelation between the time series and a lagged copy of itself

- the first line represents the autocorrelation coefficient for one time period ago

- the

blue areaaround the x-axis representssignificance, the values situated outside are significantly different from zero which suggests the existence of autocorrelation for that specific lag - the greater the distance in time, the more UNLIKELY it is that this autocorrelation persists

- e.g. today’s prices are usually closer to yesterday’s prices than the prices a month ago

- therefore, we need to make sure the autocorrelation coefficient in higher lags is sufficiently greater to be significantly different from zero

- notice how all the lines are positive and higher than the blue region, this suggests the coefficients are significant, which is an indicator of time dependence in the data

- also, we can see that autocorrelation barely diminishes as the lags increase, this suggests that prices even a month back (40 days ago) can still serve as decent estimators for tomorrow

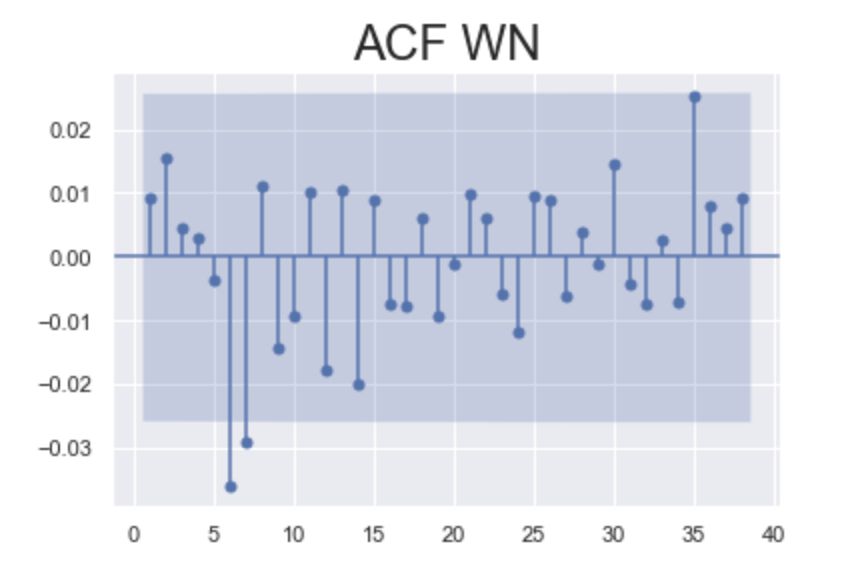

ACF for White Noise

|

|

Output:

Explanation:

- Since white noise series is generated randomly

- there are patterns of positive and negative autocorrelation

- All the lines fall within the

blue area, thus the coefficients areNOT significantacross the entire plot- No autocorrelation for any lag

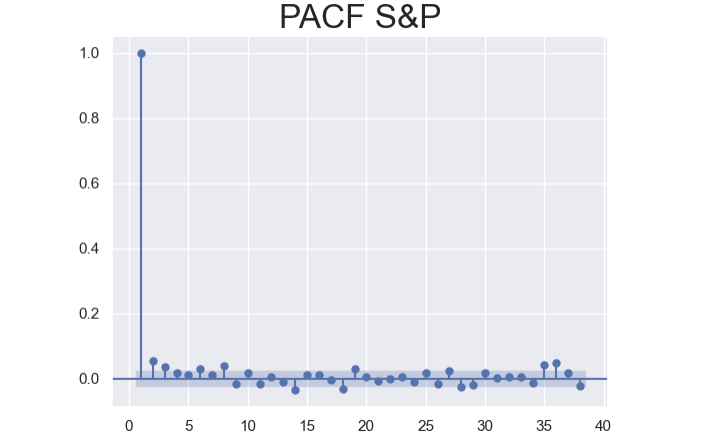

8. The Partial Autocorrelation Function (PACF)

ACF: Prices 3 days ago,

- affecting values of 1 and 2 days ago, which in turn affect present prices indirectly

- affecting present prices directly

PACF cancels out ALL additional channels a previous period value affects the present one

- $X_{t-2}$ => $X_t$

- Cancel Out: $X_{t-2}$ => $X_{t-1}$ => $X_t$

|

|

Output:

Explanation:

- PACF and ACF values for the first lag should be indentical

- Not significantly different from 0 except the first several lags

- a tremendous contrast to the ACF plot (all 40 lags are significant)

- Being positive or negative is somewhat random without any lasting effects

- negative values may be caused from Weekends.

9. The Autoregressive (AR) Model

Autoregressive Model is a linear model, where current period values are a sum of past outcomes multiplied by a numeric factor

- “autoregressive” because the model uses a lagged version of itself (auto) to conduct the regression

- use PACF to select the correct AR model because it shows the individual direct effect each past value has on the current one

- AR(2): $x_{t} = C + \phi_1 x_{t-1} + \phi_2 x_{t-2} + \epsilon_t$

- $ -1 < \phi < 1 $

- $\epsilon_t$: Residuals represent the

unpredictabledifferences between our prediction for period “t” and the correct value - More lags -> More complicated model -> more coefficients -> some of them are more likely not significant

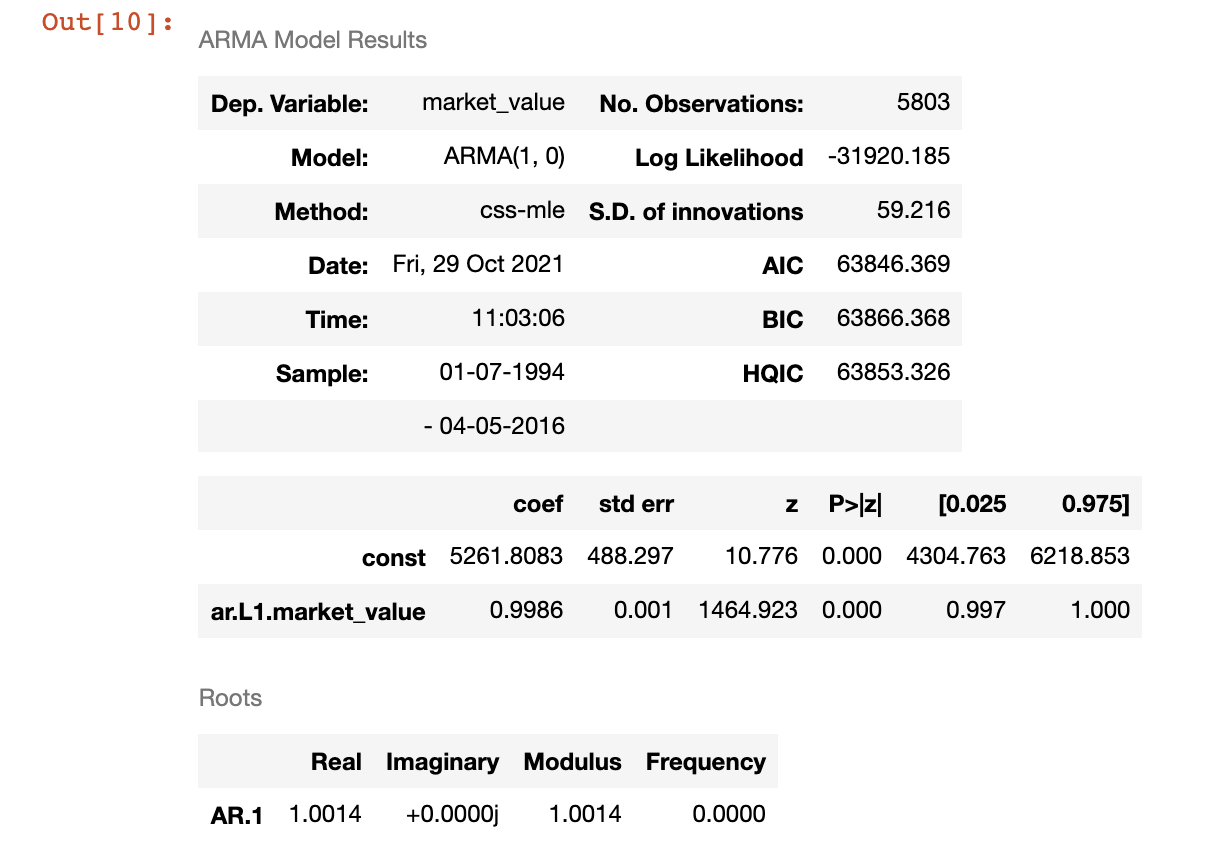

Fitting an AR(1) Model for Index Prices

Fitting the model: Find the most appropriate coefficients

|

|

Explanation:

For AR(1) Model: $x_{t} = C + \phi_1 x_{t-1} + \epsilon_t$

- C = 5261.8083

- $\phi_1$ = 0.9986

std errorrepresents how far away, on average, the model’s predictions are from the true values- p = 0 means that the coefficients are significantly different from zero

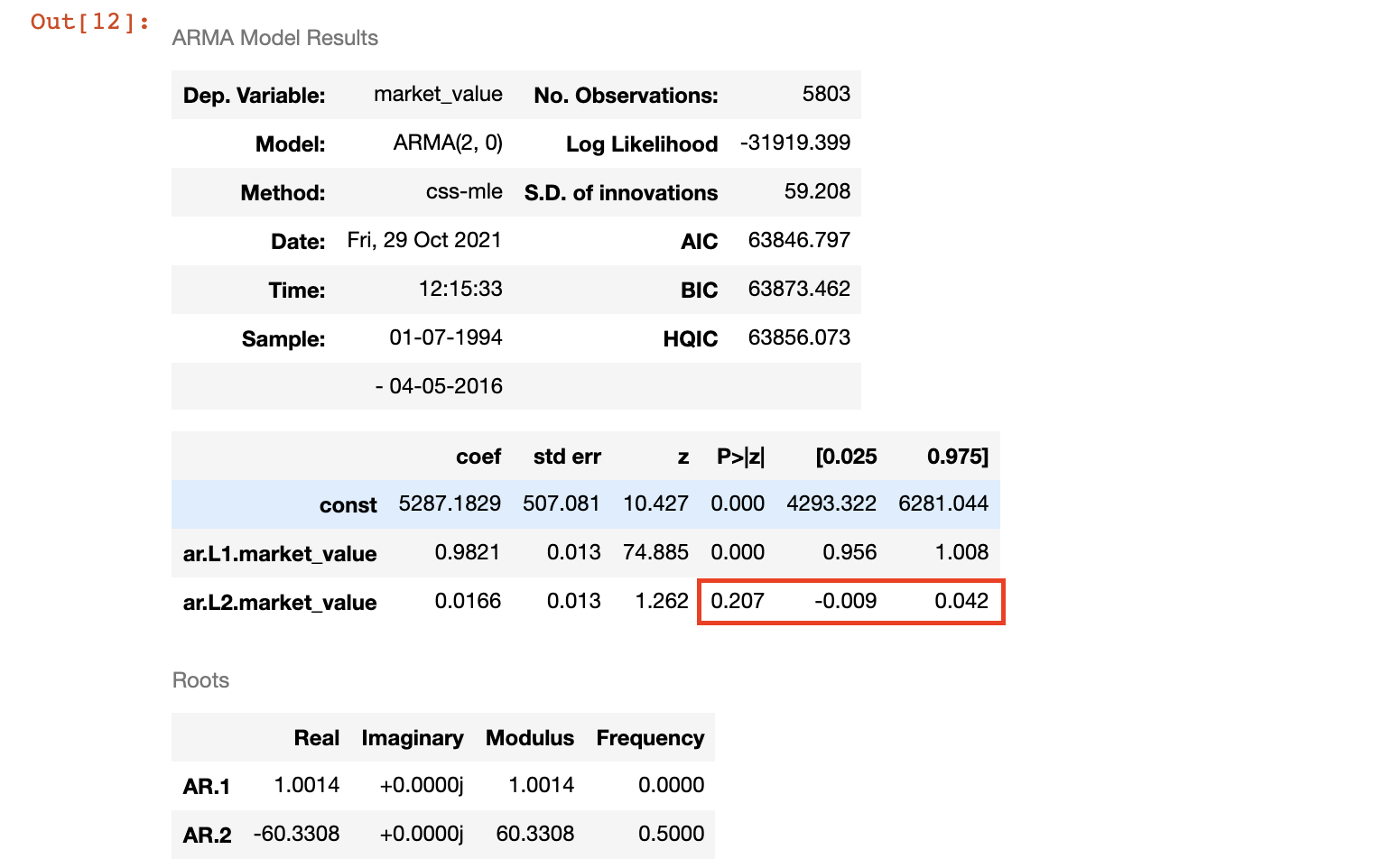

Fitting Higher-Lag AR Models and LLR

Fit AR(2) Model: $x_t = C + \phi_1 x_{t-1} + \phi_2 x_{t-2} + \epsilon_t$

|

|

- p = 0.226 > 0.05, reject the H0, $\phi_2$ is NOT significantly different from 0

- the prices two days ago do not significantly affect today’s prices

Fit AR(3) Model:

ar.L2.market_valuefrom 0.0166 to -0.0292- its p-value 0.112 is still greater than 0.05

Log Likelihoodfrom -31919.399 to -31913.087- higher Log-Likelihood => Lower Information criterion (AIC, BIC, HQIC)

Use Log-Likelihood Ratio (LLR) Test to determine whether a more complex model makes better predictions

|

|

Fitting more complicated models and checking if it gives us Distinguishably Greater Log-Likelihood, then stop before the model that satisfies:

- Non-significant p-value for the LLR Test (> 0.05)

- Non-significant p-value for the highest lag coefficient

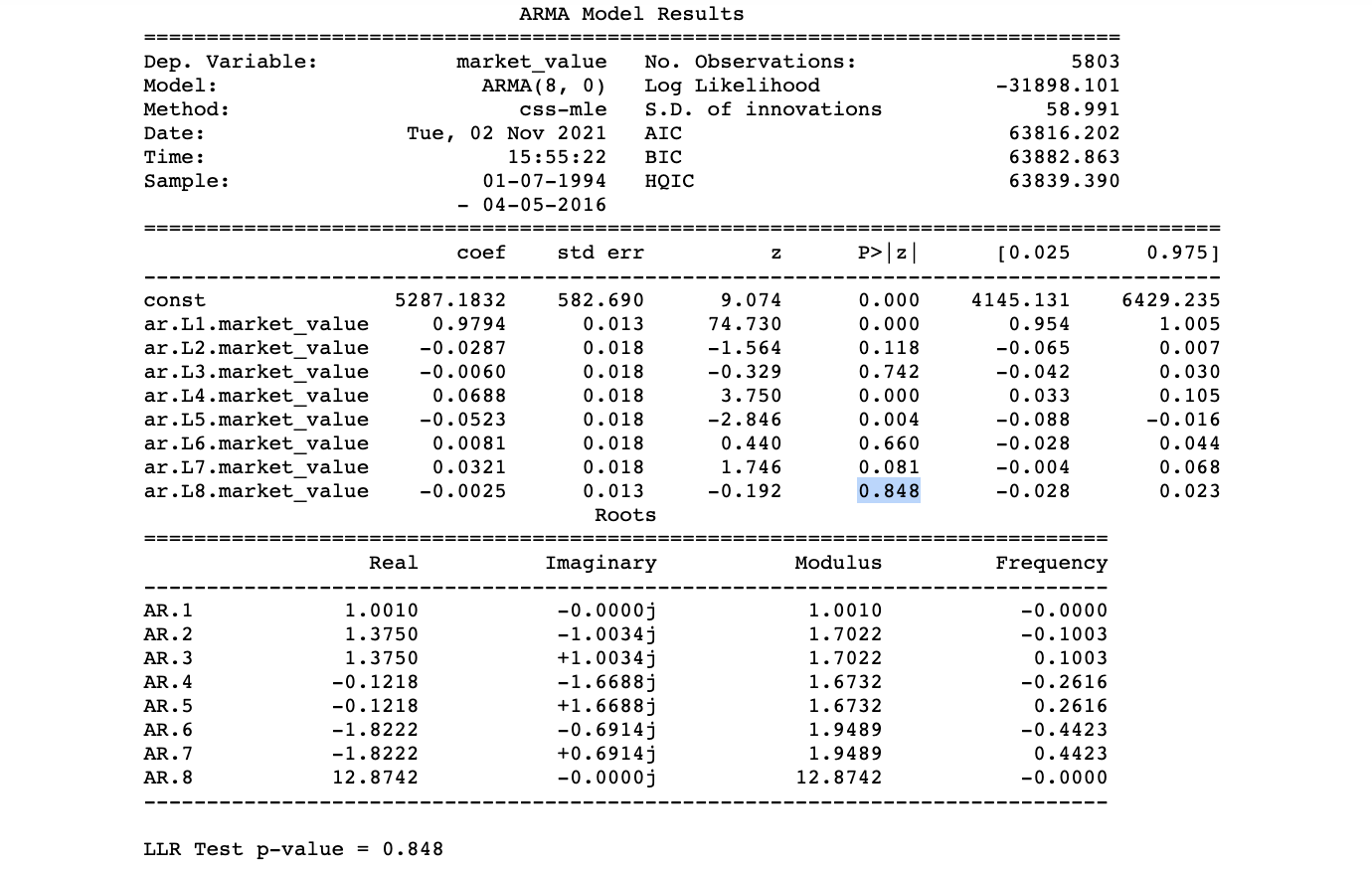

|

|

Output:

Explanation:

- AR(8) fails the LLR Test => does NOT provide significantly higher Log-Likelihood

- AR(8) has higher Information Criteria

- Including prices from eight periods ago does NOT improve the AR model

- We stop with the AR(7), even though it may contain some non-significant values

Using Returns instead of Prices

Since the market_value extracted from a non-stationary process (by DF-Test)

- we shouldn’t rely on AR Models to make accurate forecasts

- Solution: transform the data set, so that it fits the

stationaryassumptions- the common approach is to use

returnsinstead ofpriceswhen measuring financial indices returns: the % change (percentage values) between the values for two consecutive periods

- the common approach is to use

|

|

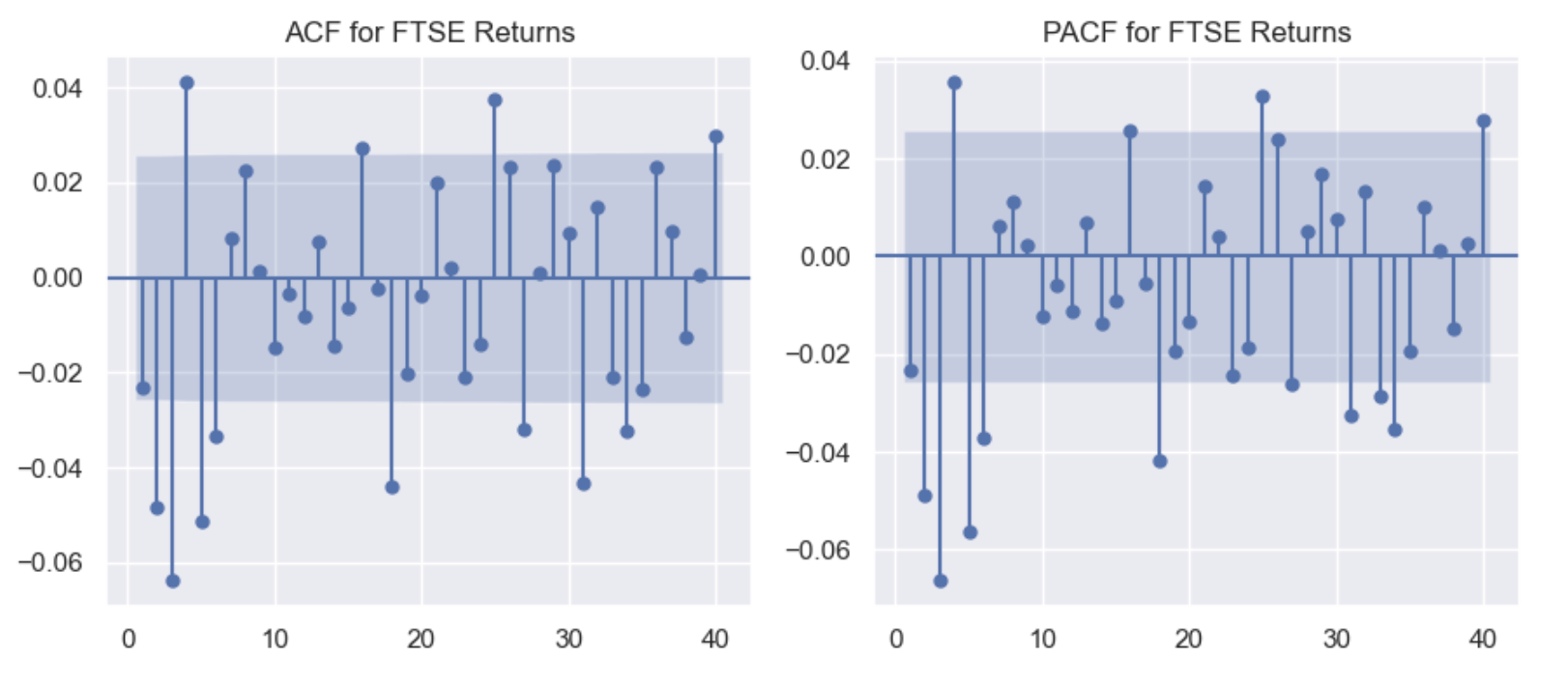

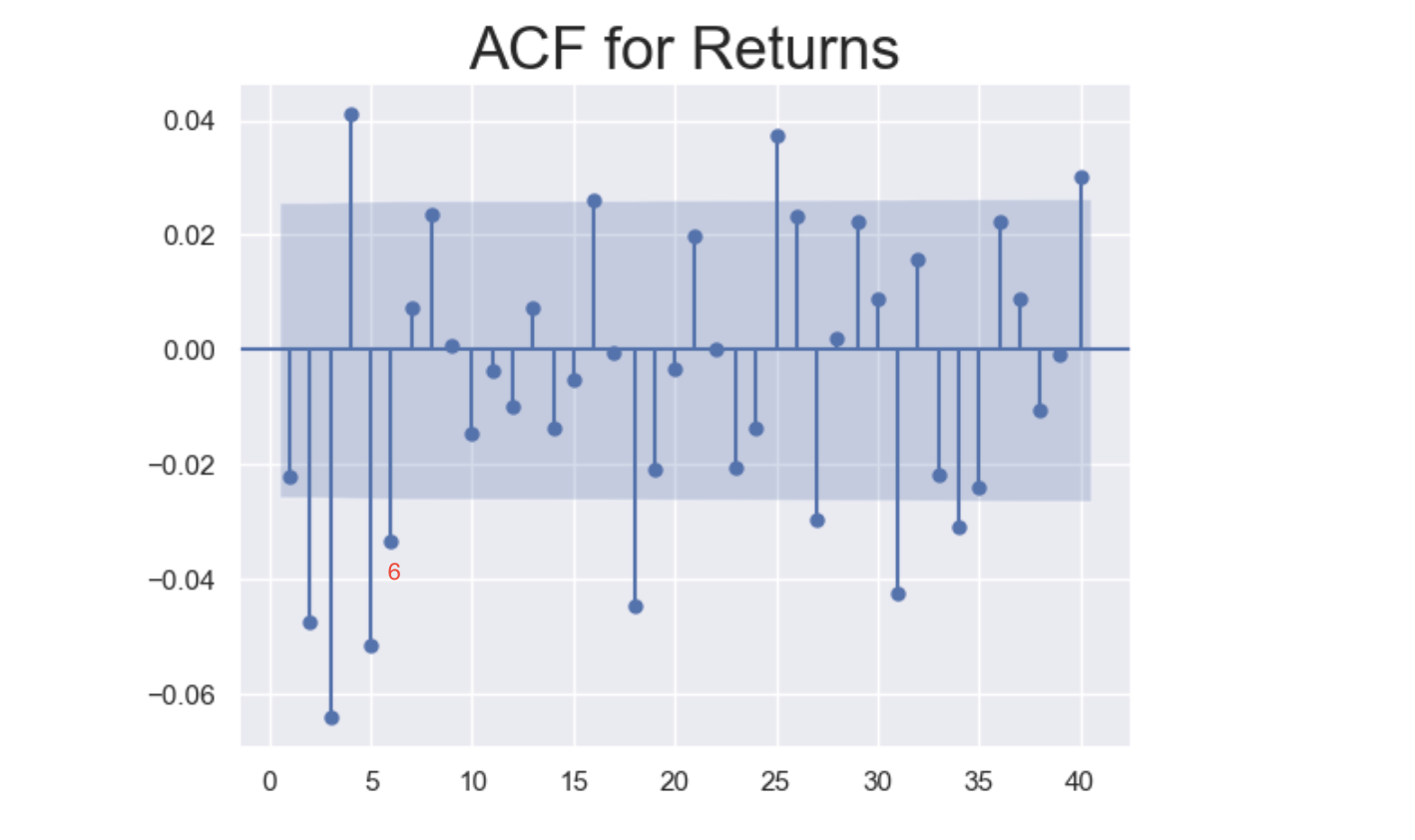

ACF and PACF of Returns

|

|

Output:

Explanation:

- ACF: Not ALL coefficients are positive or significant (as ACF for

Prices)- values greatly vary in magnitude instead of being close to 1

- Consecutive values move in different directions

- this suggests that

returnsover the entire week are relevant to those of the current one - negative relationship may have some form of natural adjustment occuring in the market

- to avoid falling in a big trend (avoid clustering)

- this suggests that

- PACF: Prices today often move in the opposite direction of prices yesterday

- Price increases following price decreases

- The majority of effects they have on current values should already be accounted for

Fitting an AR(1) Model for Returns

|

|

Fitting an Higher-Lag AR Model For Returns

|

|

Normalizing Values

Map every value of the sample space to the percentage of the benchmark (first value of the set)

- the resulting series is much easier to compare with other Time Series

- this gives us a better understanding of which ones to invest and which ones to avoid

|

|

Suppose historically, the S&P provides significantly higher returns (3%) than NIKKEI (which yields a steady 2% increase over a given period)

- then if both returns are around 3% for the period we are observing,

NIKKEIis significantly outperforming its expectations

To avoid any biased comparision when analyzing the two sets, we often rely on normalized returns

- which account for the absolute profitability of the investment in contrast to prices

- they allows to compare the relative profitability as opposed to non-normalized returns

|

|

- Normalizing does NOT affect stationarity and model selection

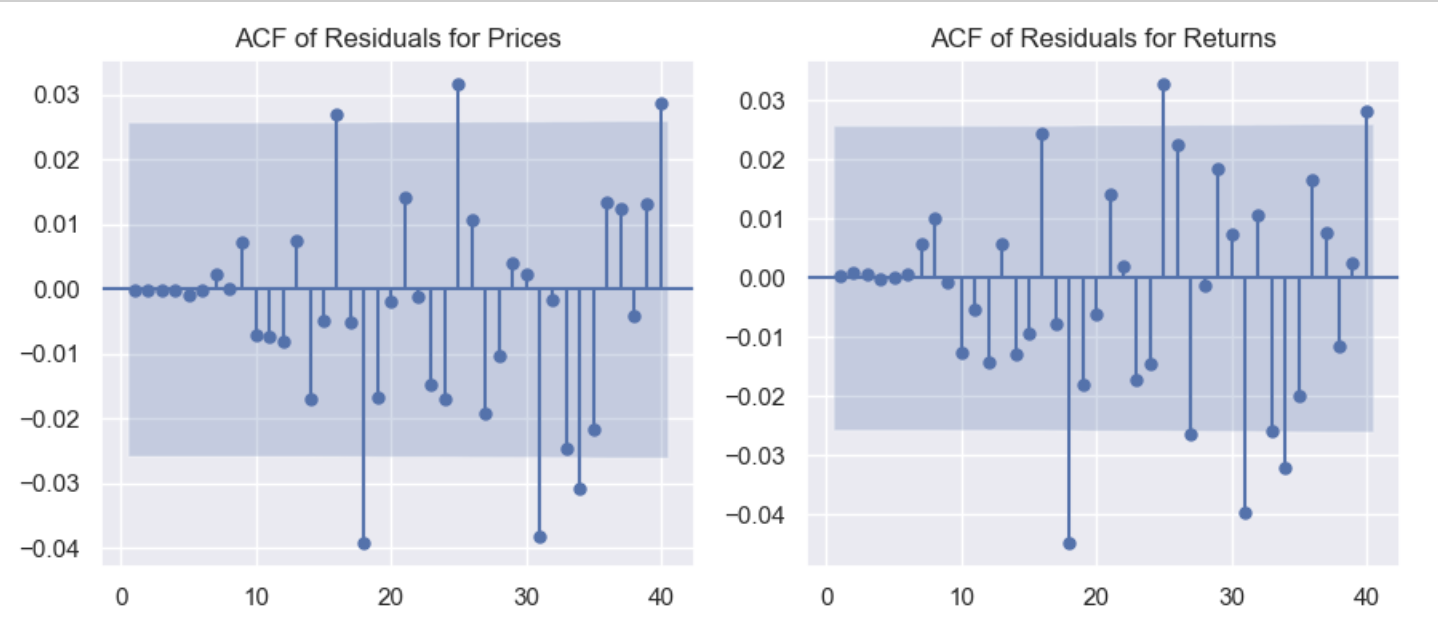

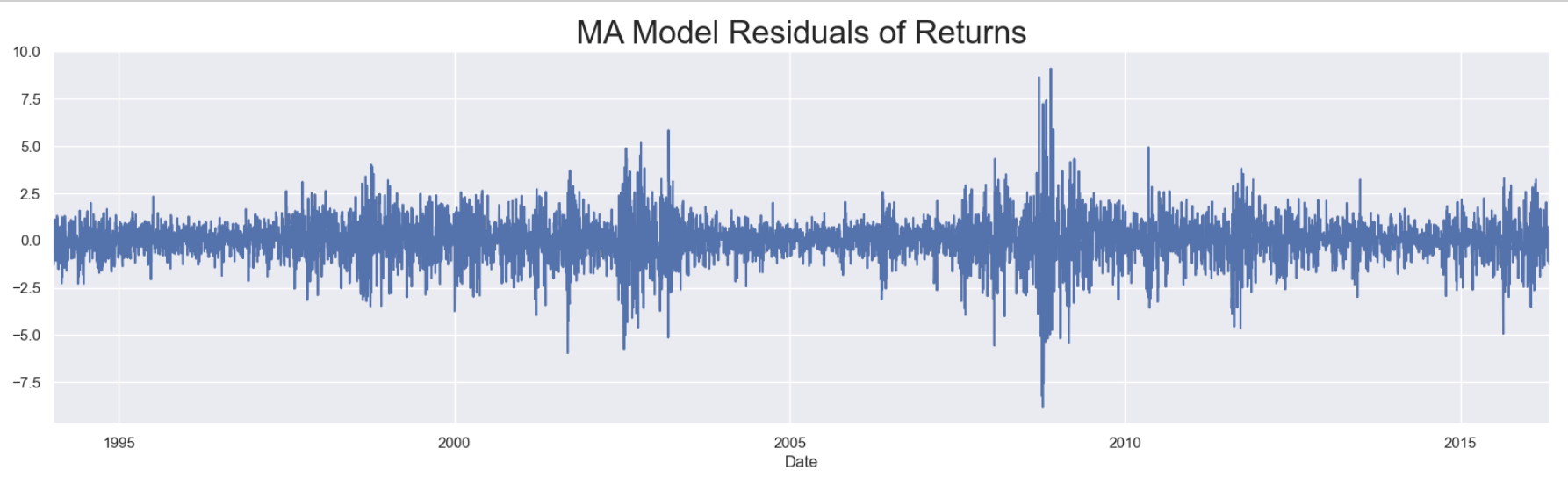

Analysing the Residuals

Ideally, the residuals should follow a Random Walk Process, so they should be stationary

Residuals of Prices

|

|

Residuals for Return

|

|

ACF of Residuals

Recall: the coefficients for the ACF of White Noise should ALL be 0

- Examine the ACF of the Residuals from a fitted model to make sure the errors of predictions are Random

- if the residuals are non-random, then there is a pattern that needs to be accounted for

|

|

Output:

Explanation:

- The majority of coefficients fall within the blue region

- NOT significantly different from 0, which fits the characteristics of white noise

- The few points outside the blue area lead us to

believe there's a better predictor

Unexpected Shocks from Past Periods

AutoRegressive Models need time to adjust from a Big, Unexpected Shock

- because AR models rely on past data, regardless of how close predictions are

There are Self-Correcting Models that take into account past residuals, adjust to unexpected shocks more quickly

- because the predictions are corrected immediately following a big error

- the more errors examined, the more adapted model is to handle unforeseen errors

Moving Average(MA) Models perform well at predicting Random Walk datasets

- because they always adjust from the error of the previous period

- because absorbing shocks allows the mean to move accordingly

This gives the model prediction a much greater chance to move in a similar direction to the values it is trying to predict

- it also stops the model from greatly diverging, which is useful for non-stationary data

10. The Moving Average (MA) Model

$$r_t = c + \theta_1\epsilon_{t-1}+\epsilon_t$$

- $|\theta_n| < 1$ to prevent compounded effects exploding in magnitude

- $\epsilon_t$ and $\epsilon_{t-1}$: Residuals for the current and past period

A Simple MA Model is equivalent to an infinite AR model with certain restrictions

- difference: MA models determine the maximum amount of lags based on ACF (AR models rely on PACF)

- becaused the MA models aren’t based on past period returns

- determine which lagged values have a significant direct effect on the present-day ones is NOT relevant

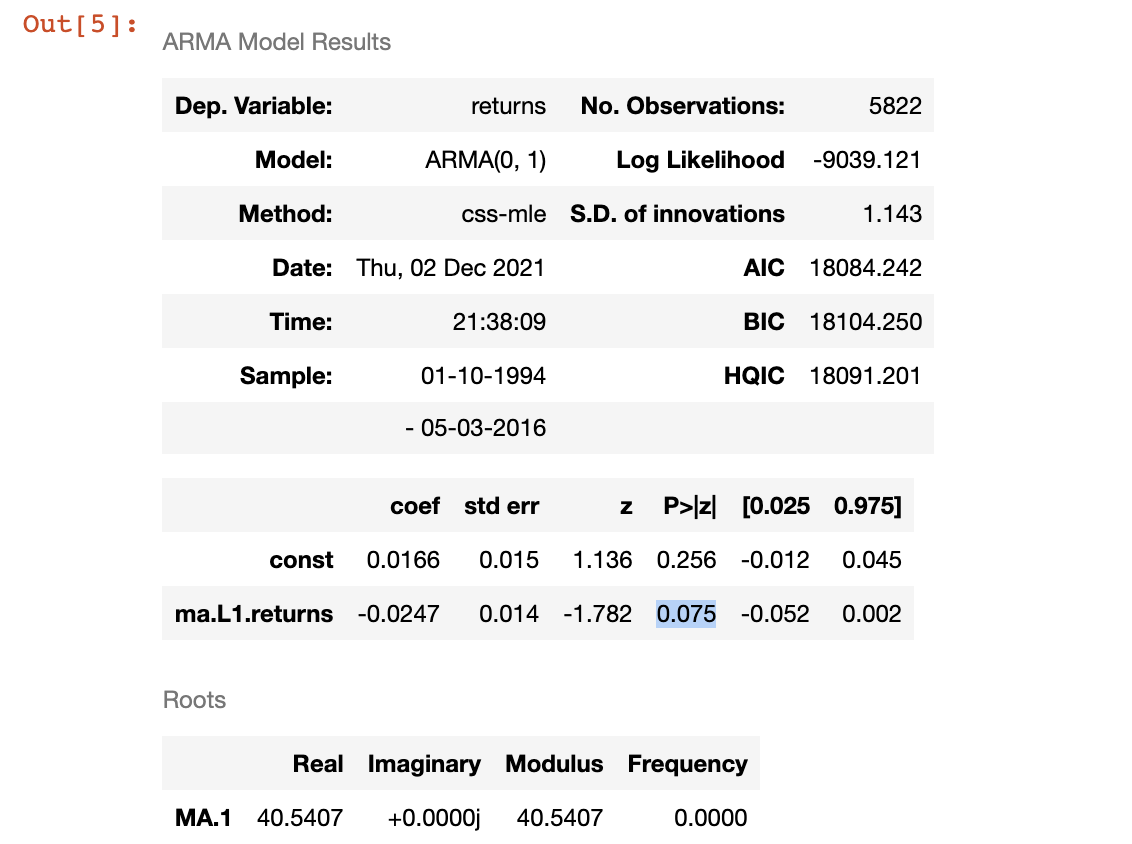

1. Fitting a MA(1) Model for Returns

|

|

Output:

Explanation:

The coefficient for the one-lag-ago residual is significant at 0.10 significant level but not significant 0.05 level

- since the first coefficient of the ACF for Returns is NOT significantly different from 0 (within the blue area)

2. Fitting Higher-Lag MA Models

|

|

ACF for Returns can give us some hints:

3. Examining the MA Model’s Residuals

We estimate the Standard Deviation of the residual, we can know how far off we can hypothetically be with our predictions

- using the 3 standard deviations rule, we can get a good idea of what interval 99.7% of the data will fall into

|

|

Output:

Exclude the .com and house price bubbles, the residuals are random

- to test if the residuals resemble a white noise process, we can check for stationary

- if the data is non-stationary, it can’t be considered white noise

|

|

Check ACF

- since a white noise process produces completely random data

- so that ACF coefficients should NOT be significantly different from zero

|

|

Output:

Explanation:

None of the first 17 lags are significant

- the first 6 coefficients are incorporated into the MA Model, so they are close to 0.

- the following 11 insignificant lags show that how well MA(6) model perform

Markets adjust to shocks, so values and errors far in the past lose relevance

- the ACF suggests that the residual data resembles white noise, which means the errors don’t follow a pattern

4. MA Model Selection for Normalized Returns

To compare different market indexes, using the normalized values is important

5. MA Model for Non-Stationary Prices

AR models are less reliable when estimating non-stationary prices